We need an updated Community Reinvestment Act that will better serve the Latino community

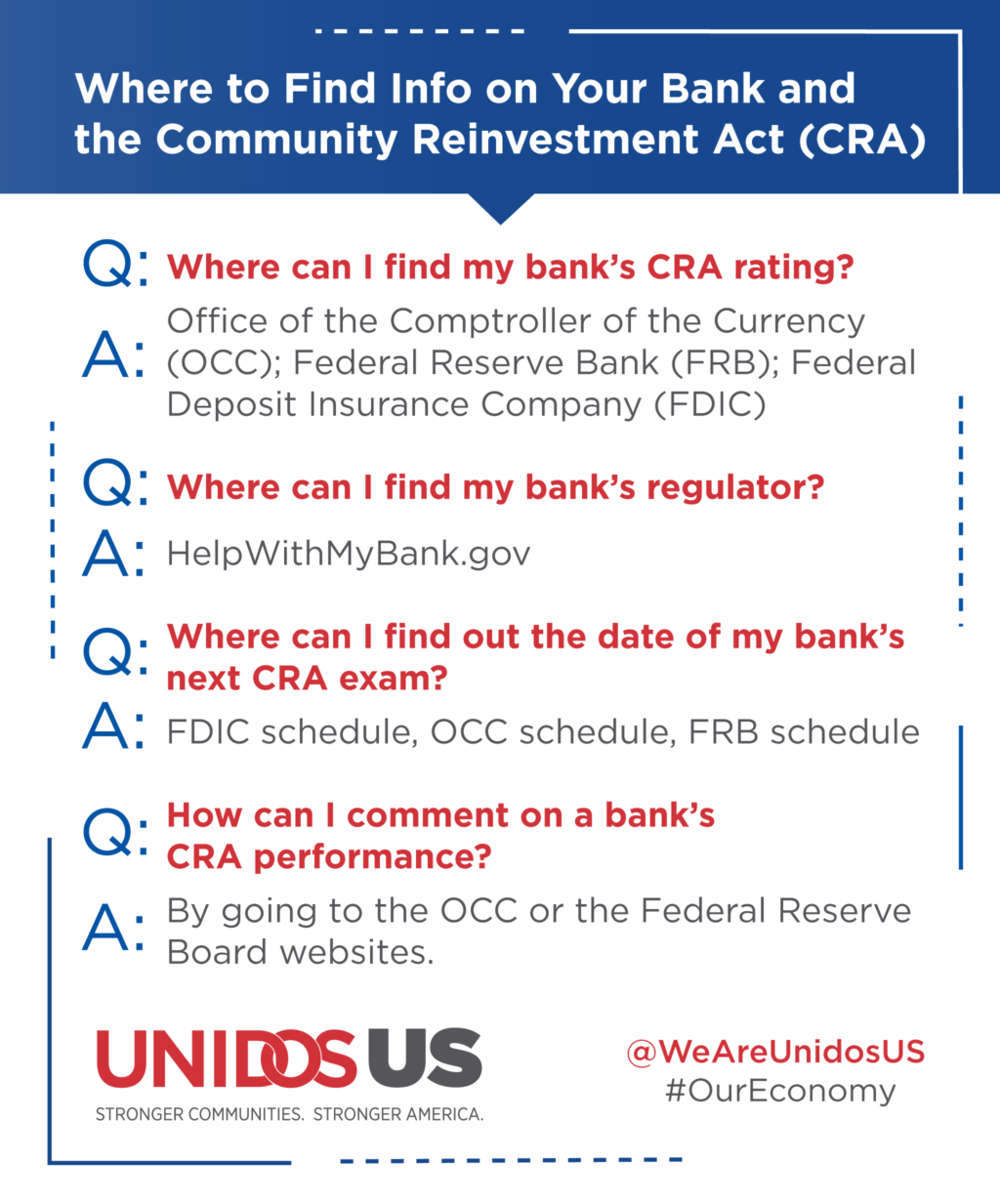

In September 2020, the Federal Reserve took the first steps towards updating the Community Reinvestment Act (CRA). It was not the first attempt in recent years to update the nearly 45-year-old civil rights law aimed at ensuring fair and affordable access to bank services, credit, and investments in low-income communities across the United States. In 2019, the Office of the Comptroller of Currency (OCC) issued its own set of guidance on the future of CRA. Yet, the OCC proposals will not strengthen the CRA and will instead have a disparate impact on Latinos and other communities of color.

The CRA is one of the most important tools used to combat the discrimination that communities of color—including Latinos—face in the banking and credit systems. Today, the CRA ensures access to banking services, capital, and credit in low- and moderate-income (LMI) communities. In the past 10 years, the CRA has contributed to the growth in Latino business ownership—an increase of 34%—by providing access to critical capital. The CRA also plays a role in ensuring that financial services available in all communities. This is important for Latinos, 14% of whom remain locked out of meaningful financial services according to the FDIC. Financial services include access to mainstream capital which 31.5% of Latino households don’t have compared to 14.4% of White households, and emergency savings rates, where only 48.2% of Latinos save for unexpected emergencies and expenses, versus the national average of 61.6%. Most importantly, the CRA helps to combat the effects of historical discriminatory housing policies, such as redlining. As such, it has promoted Latino homeownership, facilitating between 15% and 35% of home loans to Latinos since 2014.

Despite this progress, more needs to be done to address the discrimination Latinos and other communities of color continue to face in banking. The Federal Reserve’s recent proposal to modernize and update the CRA based on the existing framework is a step in the right direction. It is critical that CRA bank exams remain rigorous and evaluate the efforts by financial institutions to address discrimination in lending, while rectifying the effects of redlining, investing in community development, and expanding their presence is LMI communities. Given the growth in the community, proposals to modernize the CRA must address the banking and financial needs of Latinos.

For the CRA to meet those needs, UnidosUS believes updates must ensure:

Rigorous bank review and ratings based on bank branch presence and deposit products offered in LMI communities. Retail lending increases in LMI communities as bank availability increases. UnidosUS research shows that Latinos most commonly utilize savings accounts at a physical bank and that the number of bank branches and ATMs in a neighborhood often signal the availability of credit. Access to financial services and deposit products at full branches, staffed by customer service personnel, should continue to be weighted heavily as part of any CRA assessment.

Ratings of financial institutions are based on mortgage, consumer lending, and access to credit offer in the communities where they are located. Financial institutions that lend in the communities they know best make homeownership, entrepreneurship and even basic banking services more accessible—especially in LMI communities and communities of color. To ensure that banks lend in the communities where they are based – instead of investing solely based on profit—these institutions should receive credit for consumer lending only when they can demonstrate that their products are affordable and meet the needs of their community. Any CRA modernization efforts must ensure that LMI families are the primary beneficiaries of lending.

Review of demographic lending data be included as part of the CRA exam. Given advances in technology, collecting and reporting demographic data associated with loans to LMI individuals or communities has become less expensive and time consuming, and as such, should be included as part of CRA exams. Efforts to update the CRA must call for improvements in data collection and the creation of a database that makes determining the communities where CRA activities are happening, what neighborhoods need more focus, and to better understand if bank lending is reaching LMI and communities of color.

A bank’s fair lending record and the feedback of local communities are considered as part of the CRA exam. CRA examiners should review and weigh public comments from community organizations as part of the fair lending test. Examiners should also weigh the experiences of Latinos and other underbanked communities to determine if banks are serving the needs of the community in which they are located. Measuring a bank’s CRA activities must be done holistically and in a way that captures not only the quantity of the bank’s community involvement, but the quality.

In its history, CRA has helped to many Latinos gain access to affordable banking services as well as revitalize the neighborhoods in which they live, by facilitating access to investments large mainstream banks that may have otherwise not served them at all. Updates to critical civil rights laws like the CRA happen only once every couple of decades. UnidosUS stands ready to advocate for a strong CRA, to ensure that it is more effective in meeting the banking and credit needs of the Latino community.