Hispanics aren’t treated equally in mortgage lending—better data could change that

By Stephanie Presch, Content Specialist, UnidosUS

In May 2019, UnidosUS Affiliate Latino Leadership and UnidosUS subsidiary Hogar Hispano in Orlando, Florida, teamed up with JPMorgan Chase to give a home to a family that had fled Puerto Rico in the aftermath of Hurricane Maria, enabling them to become homeowners in the United States.

After the hurricane struck, Juan Carlos and Jinny Santos didn’t have access to food, and both water and power services were lacking on the island. When they decided to move to the United States, two of their daughters were sick, and Jinny was pregnant. When they arrived in Orlando, they were living in a FEMA hotel as they tried to settle into their new lives.

The story of Juan Carlos and Jinny’s family underscores how important data is to help advocates, researchers, and policymakers explain differences in the experience that Latino subgroups have in the mortgage market.

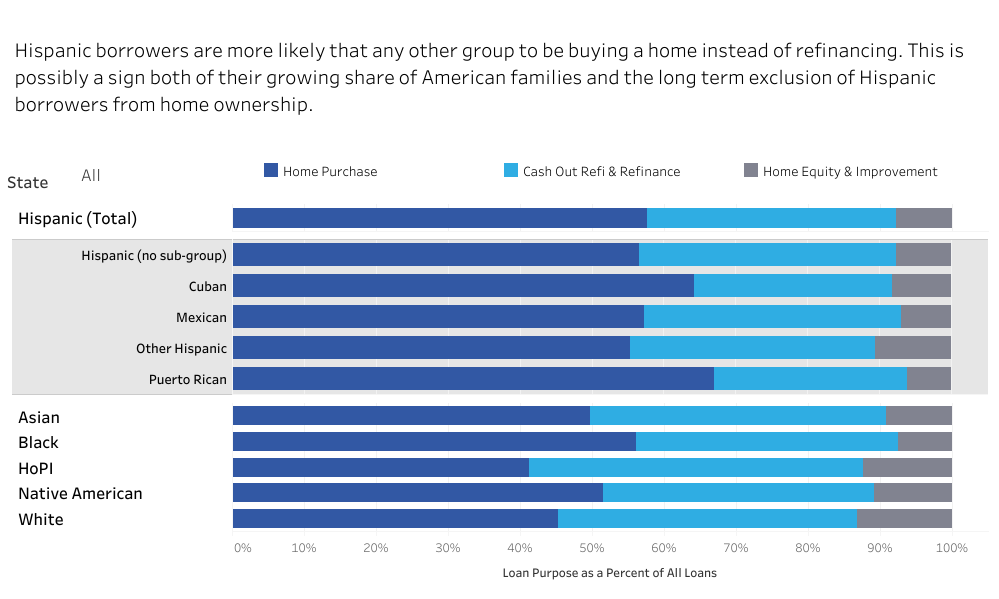

In 2019, more than 470,000 Latinos became homeowners. More than half (58%) of the loans that Hispanics received that year were to help them buy a home, which was higher than the percentage received by non-Hispanic Whites nationally. However, since the beginning of the coronavirus crisis in March 2020, Latinos have disproportionately lost jobs and income during the pandemic, and many are at risk of losing their homes.

However, this portrait of homeownership in our community is incomplete.

A new report by UnidosUS and the National Community Reinvestment Coalition presents data on mortgage lending patterns for Latino borrowers, highlighting nuances in home lending among Cuban, Puerto Rican, Mexican, and Afro-Latino borrowers. This is significant, because while one in three Hispanic borrowers overall relied on government-insured loans in order to buy a home, when the data was separated out by ethnicity, more than half—52%—of home loans to Puerto Ricans were insured by the federal government. Even between 2000 and 2010, homeownership rates among Hispanic subgroups varied. For example, the rate for Cubans decreased by less than one percentage point, whereas homeownership increased by 10 percentage points for Salvadorans.

Additionally, this report highlights where Afro-Latinos are applying for a home loan, and where they are becoming an influential part of the housing market. While there is little research on Afro-Latinos’ experience with homeownership, there is some data from the that suggests that Afro-Latinos experience higher rates of discrimination in comparison to non-Black Latinos. A report by UnidosUS in 2017 even indicates that Afro-Latinos experience higher rates of unemployment and poverty than non-Black Latinos.

Even though Latinos made significant progress last year in becoming homeowners, 20% were still denied a loan when they applied. This figure was 43% higher than the denial rate for non-Hispanic Whites who applied. Latinos were also charged more than non-Hispanic Whites for the loans that they did receive, which also affects their ability to build home equity over time.

Federal policymakers and lenders must take into account Latinos’ diverse needs when shaping housing policy and mortgage programs. With more accurate information, organizations like the ones in our Affiliate Network, as well as policymakers—will be able to better assist Latinos in accessing mortgages and affordable homes, especially once our nation begins on a path to recovery from the coronavirus crisis.