Unscoreable: Modern-day credit scoring leaves Latinos and immigrants out

Today’s credit system fails to include one in 10 American adults, leaving 45 million Americans “credit invisible.”

A person is “credit invisible” when she does not have a record of credit with one of the three largest credit rating agencies in the United States: Experian, Equifax, or TransUnion. For almost the 20% of Americans who are credit invisible, it’s more difficult to buy a home, more expensive to turn on utilities, and harder to get a job.

And while the credit system touches the lives of all Americans, it leaves out many Latinos and immigrants. Latinos are almost twice as likely to be credit invisible than Whites.

It’s time for this system to evolve.

“[A] high credit score opens the door; a low credit score, they take away the keys.”

— Dolores from Pennsylvania

Latinos and communities of color have long been at a disadvantage in the U.S. credit system. In the 1930s, Homer Hoyt, once the chief economist of the Federal Housing Authority, created a risk hierarchy that labeled Latinos as “too risky” for home mortgage lending. This created a foundation for redlining policies, which granted White individuals and families access to safe and affordable credit while keeping out people of color.

These racially driven policies made it difficult for Hispanics to borrow from banks. But this is not all in the past. Despite improvements made by laws like the Community Reinvestment Act, Latinos continue to face limited banking options today, and are more likely to live in neighborhoods with fewer bank and credit union branches.

“My experience with not having credit has been bad and sad. When I went to the car dealership to try to purchase a new vehicle, I was denied a car loan because I don’t have credit. Since I don’t have a Social Security Number, I have tried to build my credit by using my Individual Taxpayer Identification Number but not all lenders accept it or can’t see the history of my activities. I feel that my work and work history should be the factor that determines if I get a loan; if I have income coming in at the end of the day I will be able to make the loan payments.”

—Miguel from California

Having fewer banks in the neighborhood is not the only reason Latinos are credit invisible. The current credit system does not take into account cultural norms.

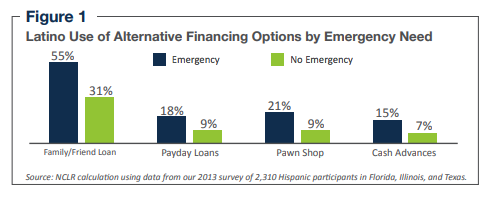

While many Latinos use non-traditional lenders to obtain a loan, many also simply choose not to borrow at all. In a 2013 survey by UnidosUS, 64% of Latinos said they used cash for everyday transactions and 61% used a debit card.

Additionally, many Latino immigrants have recently moved to the United States, which means that they lack the credit record and information necessary to gain access to credit.

Time for an evolution

It’s time for the current system to evolve, especially given the economic importance of our nation’s 58.8 million Latinos. The current system relies on formulas and algorithms that were created by for-profit companies that fail to account for a variety of ways that people make on-time payments.

“Credit bureaus are the original gangsters because they have their own system.”

—Carla from Pennsylvania

According to the credit scoring company FICO, 35% of an individual’s credit score is based on records of on-time payments. However, it does not take into account on-time utility payments, phone or cable bill payments or remittances, which if used, could open the door for many more Latinos.

Determining a person’s creditworthiness in this way would not mean that riskier people get credit; instead it would allow banks to gain a better, more accurate picture of a person’s ability to pay a loan, including millions of Americans who are currently rendered invisible.

UnidosUS will continue to advocate for fixing the credit scoring system so that it is not largely associated with income and wealth, further perpetuating the racial wealth gap. We will work closely with policymakers and federal agencies to create a more inclusive system for communities of color, in low-income neighborhoods, young Americans, and immigrant communities.