FHFA Takes Key Step to Improve Language Access in the Mortgage Market

Last week, the Federal Housing Finance Agency (FHFA) made a key decision to include a question that asks a borrower his or her preferred language on the updated standard mortgage application. We and our partners in the civil rights community applaud this critical fix to the mortgage application process.

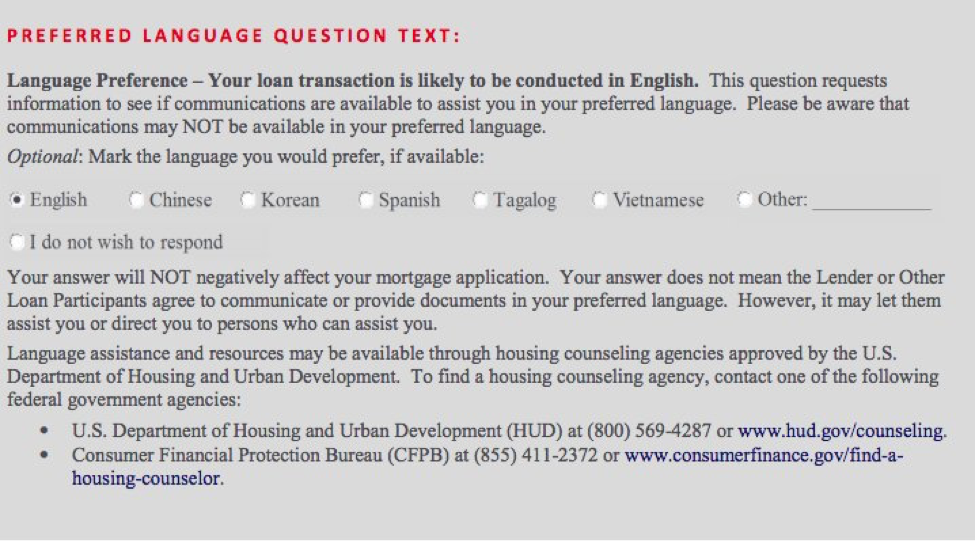

This is how the question will appear on the updated mortgage application:

WHAT’S YOUR LANGUAGE PREFERENCE? A SIMPLE YET POWERFUL QUESTION

This decision has been years in the making. In 2015, Fannie Mae and Freddie Mac, two large companies that buy and securitize loans made by home lenders, announced that they would be updating the mortgage application for the first time in 20 years. FHFA, as regulator and caretaker of the companies, met with different stakeholders, including UnidosUS, to get feedback on the process.

We joined consumer advocates in the Americans for Financial Reform coalition to request that FHFA include a question on the re-designed mortgage application asking borrowers to indicate their preferred language.

In the last two years, we advocated for opportunities to track and collect information about a borrower’s language preference. Additionally, we proposed ideas for how home lenders and mortgage servicers could improve access to credit and mortgage relief options for Latinos and other underserved borrowers with limited English proficiency.

After many meetings, submitting our recommendations, conducting surveys, and developing best practices with Affiliates in the UnidosUS homeownership network, we applaud FHFA for taking this important step to improve language access in the mortgage market.

HOMEOWNERSHIP CHALLENGES FOR AMERICANS WITH LEP

Several factors, including language ability, can impair the ability of Hispanics to access and understand credit. The mortgage market is aimed primarily at English-language speakers. But more than 60% of Americans with limited English proficiency speak Spanish, and nearly 65% of Latino immigrant families identified as limited English proficient (LEP).

The challenge of navigating the complex mortgage process is compounded for LEP families. Often LEP borrowers enter into mortgage loans without understanding the terms of the contract due to the lender’s failure to provide communications in a language they can understand. And the lack of language assistance services puts many borrowers at a tremendous disadvantage when seeking mortgage relief to save their home.

While Latinos and immigrants with limited English proficiency encounter barriers to safe credit products, they are also vulnerable to fraud and predatory practices. Identifying that a borrower or homeowner would benefit from language assistance services or from a bilingual service provider would protect these families from financial traps and ensure access to sustainable homeownership, a key building block to create wealth.

NEXT STEPS IN IMPROVING LANGUAGE ACCESS

Including this particular question on mortgage applications is a step in the right direction to ensure that Latinos, immigrants and other underserved communities with limited English proficiency have access to safe and affordable mortgage products. The next step is for Fannie Mae and Freddie Mac to develop a comprehensive language access plan.

The updated mortgage application will be finalized later this year. By 2020, families who apply for a home mortgage will be asked this question when completing the mortgage application.

We will continue to monitor the development of the language access plans enabling more American families, including Latinos and immigrants, to secure homeownership opportunities.

FIND OUT MORE