Access to Small-Dollar Credit Leads to Immigrant Financial Inclusion

By Sabrina Terry, Senior Strategist, Economic Policy Project, NCLR

The size of the U.S. immigrant population has grown significantly over the past 40 years, from 4.7 percent of the total population in 1970 to 13.5 percent in 2015. Of the 43 million immigrants living in the United States in 2015, 45 percent (19.5 million) were Latino. The hard work and ingenuity of the immigrant community has produced many important contributions; for example: the foreign-born labor force participation rate (65.2 percent) exceeds that of native-born workers (62.2 percent); immigrants are more than twice as likely to start a business as native-born citizens; and foreign-born Latinos who have become naturalized citizens vote at higher rates than native-born Latinos.

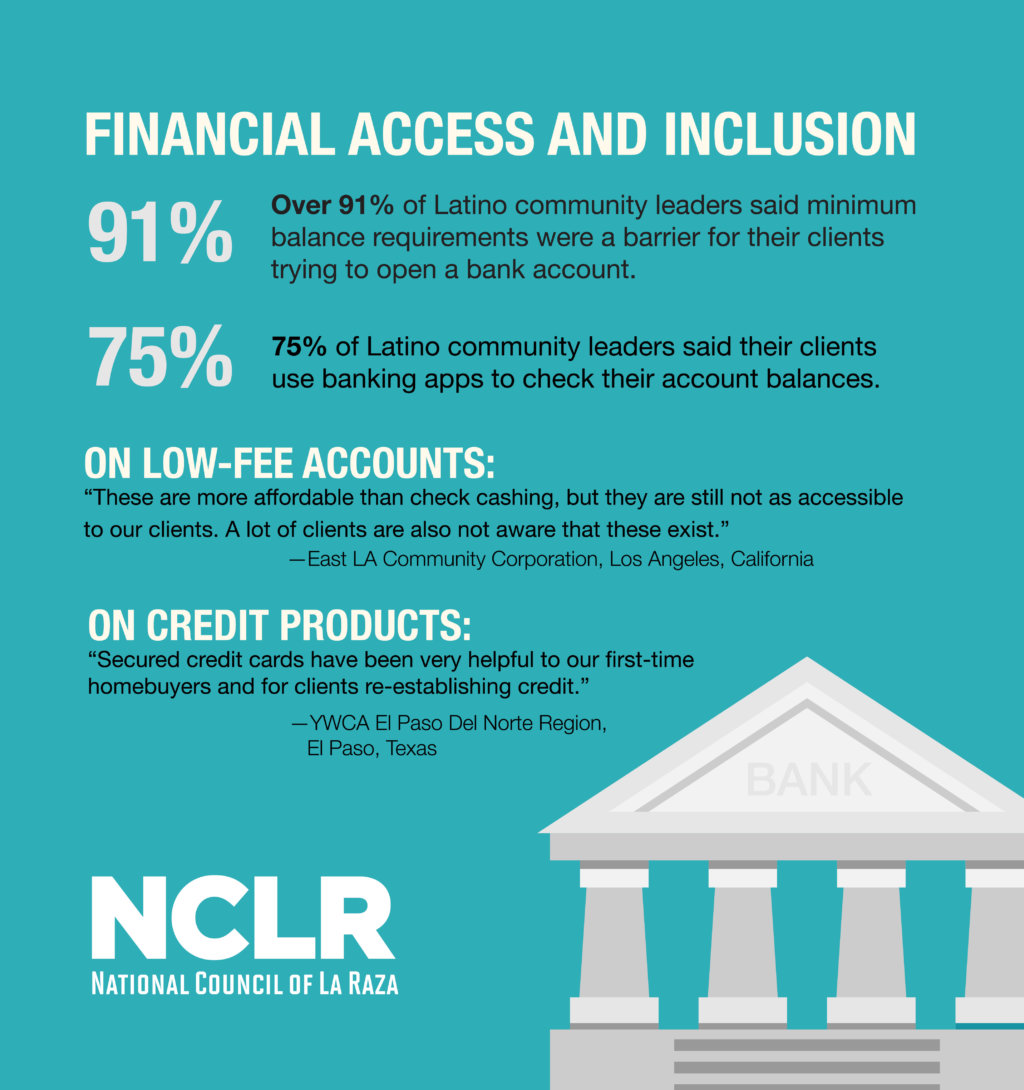

Yet there are also areas where immigrants lag behind their native peers, and targeted interventions are needed to help people fully integrate into American society. One such area is financial inclusion, the ability to access and utilize affordable financial services and products, which is essential to building a financial identity, assets, and wealth in this country. Many Latino immigrants lack knowledge of how to navigate the U.S. financial system. In addition, immigrants tend to have unique financial backgrounds—uneven income streams or cash income, less likely to be banked, and more likely to have thin or no credit histories.

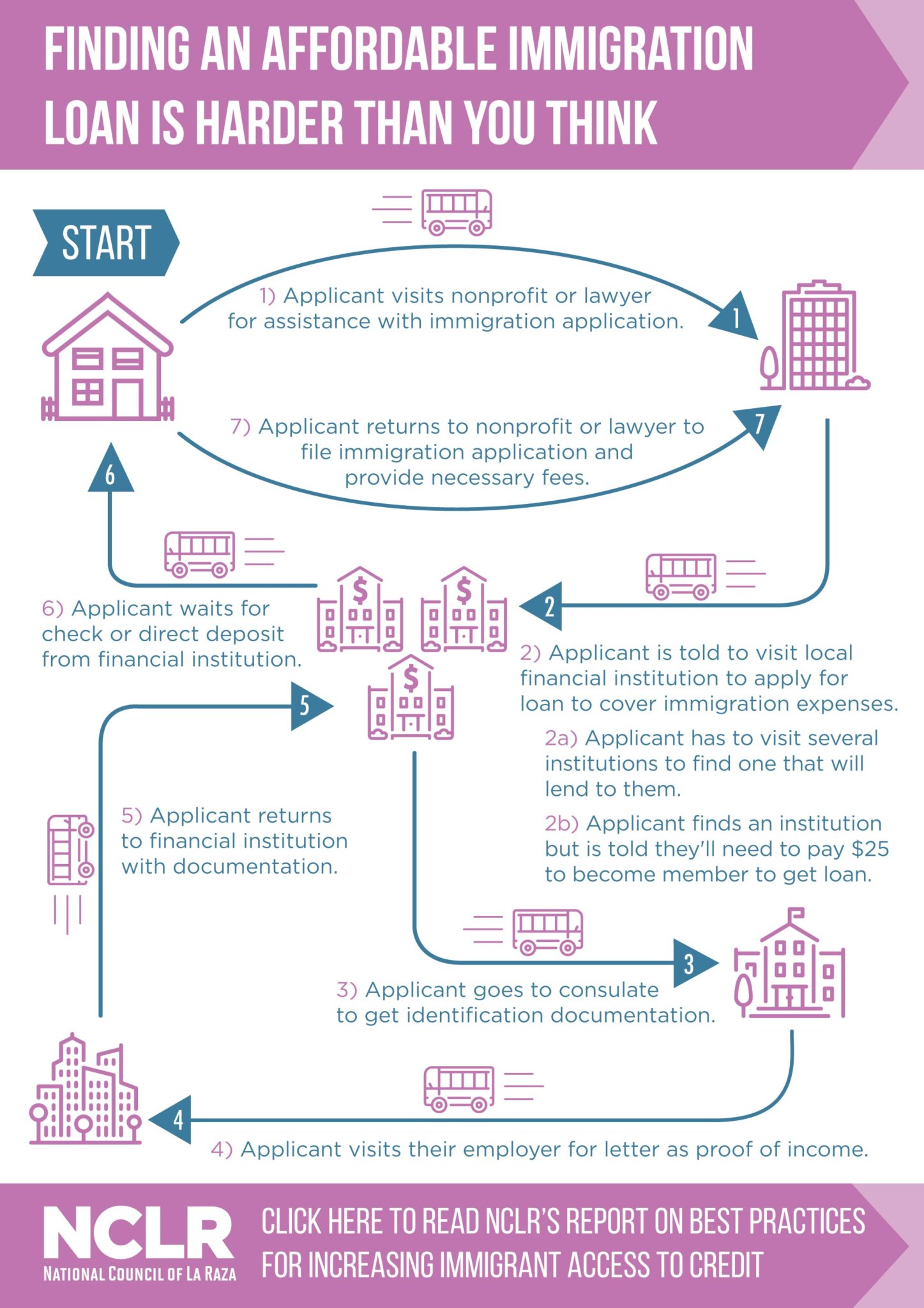

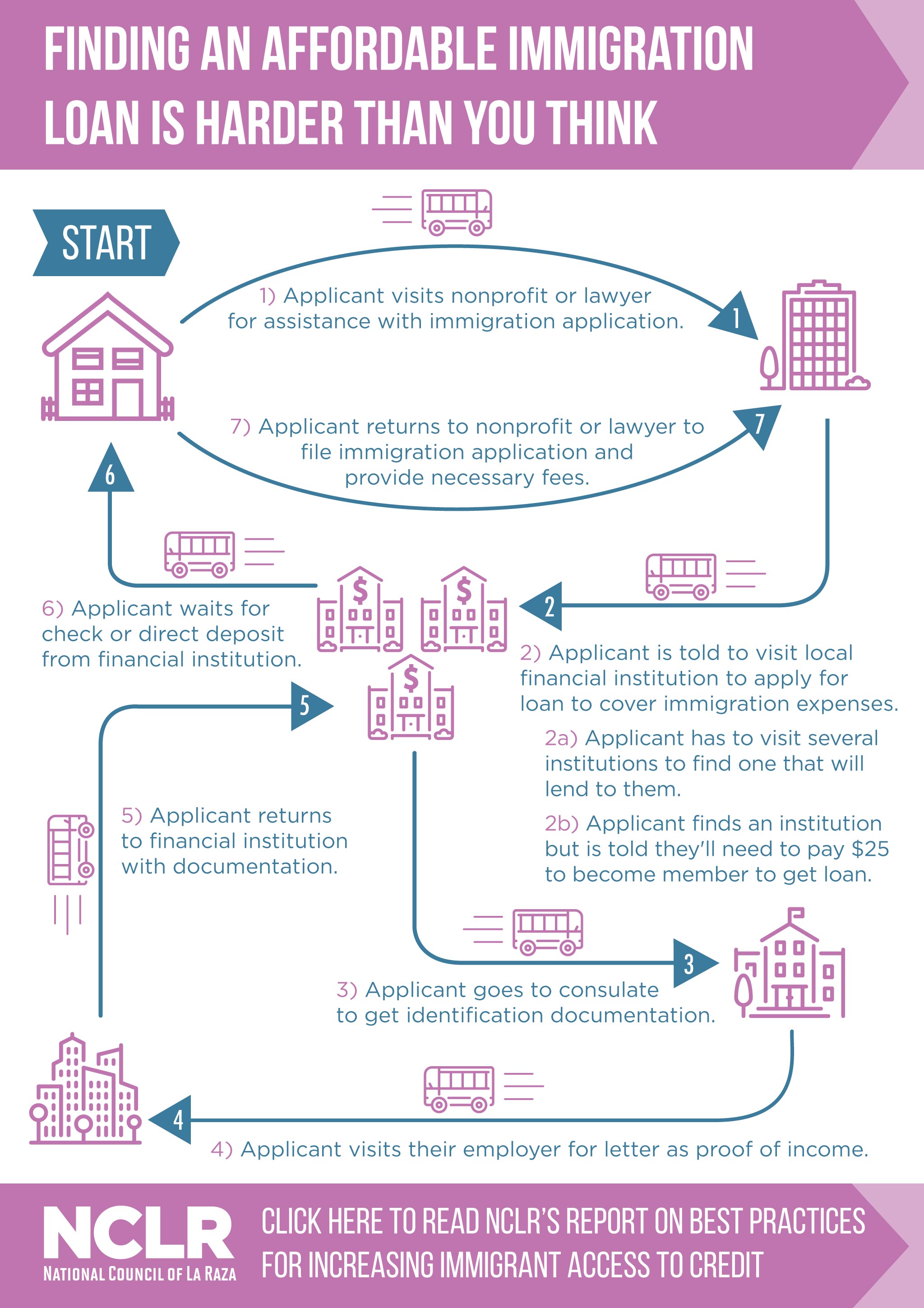

An ability to overcome these financial barriers is critical to an immigrant’s journey toward citizenship, since the process is expensive. In fact, naturalization application costs have ballooned 545 percent since 1995, growing from $95 in 1994 to $640 in 2017 (which does not include the $85 biometric fee that an applicant must pay). Other immigration status change application fees are even higher—ranging from $500 and $5,000—which doesn’t include additional expenses like English classes, legal aid, or civics test preparation.

A new report from NCLR, Small Dollars for Big Change: Immigrant Financial Inclusion and Access to Credit, takes a deeper dive into what solutions might exist to help immigrants who are ready to adjust their status but need help financing the process with small-dollar credit options. The report, produced with support from Citi Community Development, identifies innovative solutions for increasing immigrant financial inclusion and promising approaches to expand the availability of small-dollar credit products that are mainstream and affordable instead of predatory. NCLR’s recommendations for going to scale with products that are affordable for Latino families and profitable for financial institutions include:

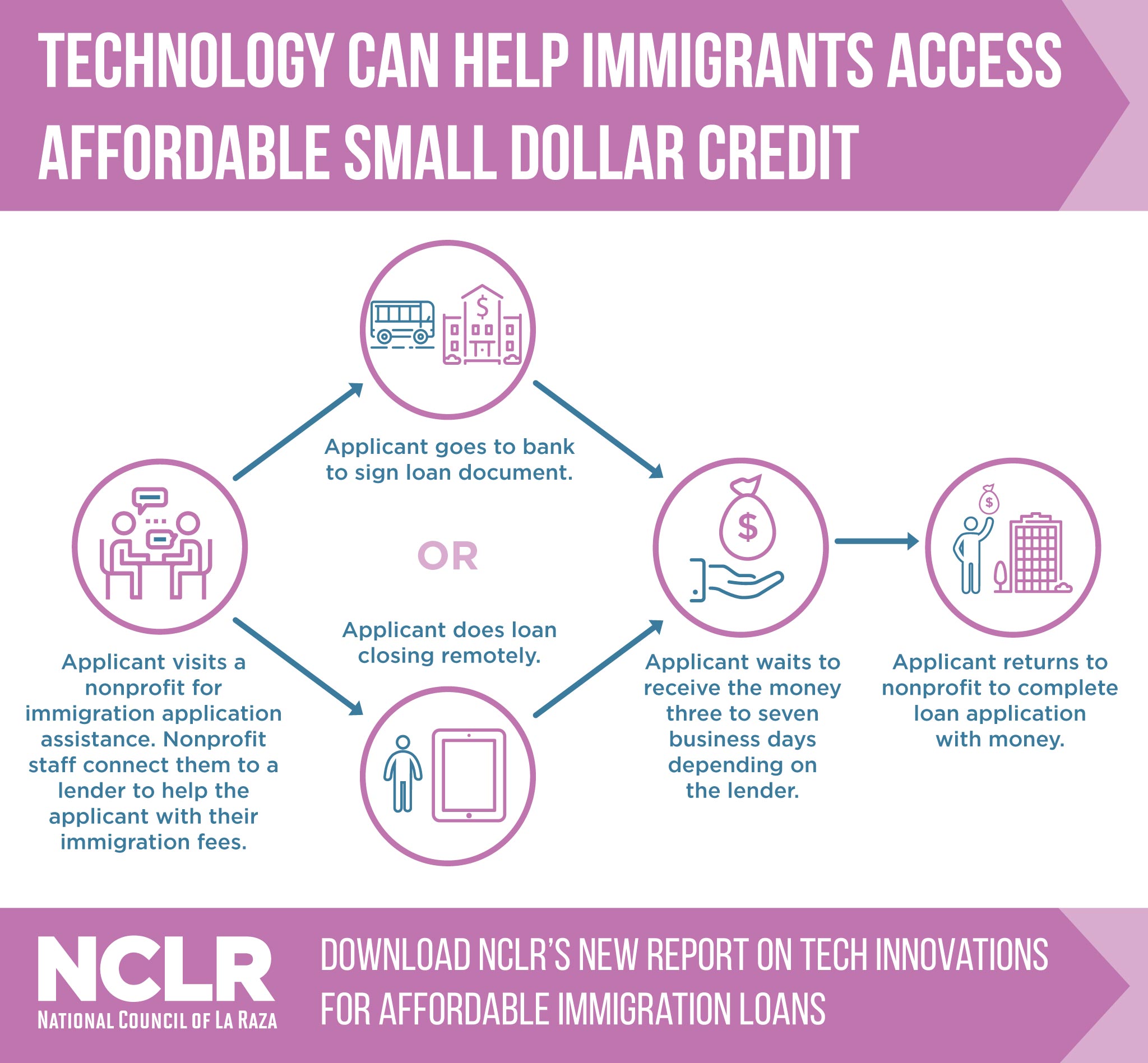

- More lender technology enhancements. A key to decreasing the costs associated with small-dollar loans is using technology to facilitate the application and decision-making process. More investments like this must be made across different financial institutions to better serve the growing Latino community, who are the highest users of mobile technology.

- More lenders focused on immigrant financial needs. Financial institutions have an opportunity to fill a critical void in the small-dollar market with loans ranging from $500 to $5,000. Helping an immigrant with their immigration status change might only generate small profits in the short-term, but providing affordable loans will create loyalty and allow lenders to build a deeper relationship with these customers over the long-term.

- Better integration between financial services and immigrant-serving programs. Legal service organizations are a critical gateway to the immigrant community because they are trusted sources of information and can break down cultural misconceptions that immigrants may have about debt and loans. Financial institutions can benefit from partnerships with legal service providers to expand their name recognition into immigrant communities and capture referrals that bring down their customer acquisition and loan origination costs.

Facilitating newcomers’ integration into the American mainstream is beneficial to our nation, and access to safe and affordable loans is an important stepping stone toward immigrant financial inclusion, credit-building, and ultimately long-term economic stability. Market interventions that combine financial inclusion and affordable credit products are widely beneficial and more sustainable than approaches that separately attempt to tackle the problems of immigrant financial capability and lack of legal status or citizenship. Now is the time to think critically about how to scale systems that make affordable products widely available since they have the potential to accelerate immigrants’ integration into U.S. society.