Spotlight on Hispanic Households: Results from the 2015 FDIC Survey of Unbanked and Underbanked Households

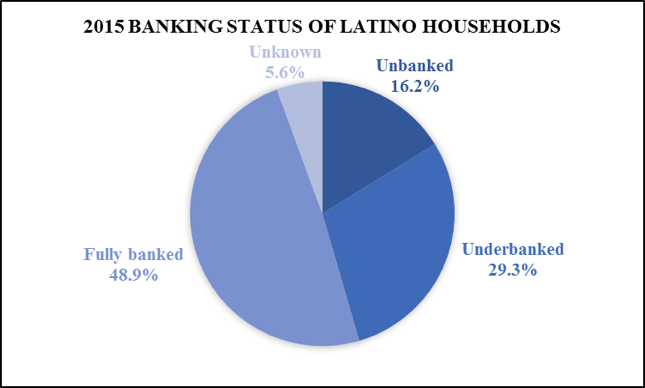

Latinos were less likely to be unbanked in 2015 than they were in 2013, meaning they didn’t have a checking or savings account. The Hispanic unbanked rate in 2015 was down 1.7 percentage points from 2013, representing approximately 273,000 Latino households that were now either underbanked (they have bank accounts but also use other services like prepaid cards or payday loans) or fully banked. This positive finding comes from the FDIC’s 2015 Survey of Unbanked and Underbanked Households.

Although it is good news that fewer Latinos were unbanked, bank accounts alone are not a silver bullet to financial inclusion, as found in the Banking in Color report. Co-authored by NCLR, the report provides findings from a survey of low- and moderate-income communities of color on their levels of financial engagement. As both the FDIC and Banking in Color reports illustrate, longstanding barriers to accessing safe and affordable financial services and products continue to affect Hispanics’ overall economic well-being and include:

- An increase in the share of underbanked Latino households. In 2015, 29.3% of Hispanic households were underbanked compared to 19.9% of all households. Between 2013 and 2015, there was a nearly one percentage-point increase in the number of underbanked Latino households. By 2015, the number of underbanked Latino households stood at 4.7 million.

- Hispanics were more likely to say that banks were not at all interested in serving households like theirs. Nearly a quarter (23.3%) of Hispanic households thought banks were not at all interested in serving households like theirs. This figure is considerably higher than both the overall and White household rates of 15.8% and 12.9%, respectively. Banking in Color found that customer service, as well as the ability to communicate in their native language, is a determinant factor when a person of color is deciding where to bank. These findings, from both Banking in Color and the FDIC survey, indicate that personal engagement with a financial institution can greatly influence the overall experience and perceptions of institutions for Latinos and other underserved consumers.

- Latinos applied to bank credit at lower rates and had higher application denial rates. In 2015, 11.5% of Hispanic households applied for bank credit, compared to 13.9% of overall U.S. households and 14.9% of all White households. In 2015, 3.6% of Hispanic households were denied bank credit, compared to 2.8% of U.S. households and 2.6% of White households. Additionally, the bank credit denial rate among Hispanics was the highest of any racial or ethnic group. Among Latino respondents from a 2013 NCLR survey, nearly half (44%) of Latinos reported they did not own a credit card.

Recent polling from NCLR on Latino perceptions of the economy are also consistent with FDIC findings. NCLR’s new economy poll based on a nationwide survey of 1,000 registered Latino voters found that 67% of respondents believe Hispanics encounter discrimination when applying for loans or credit, or dealing with financial institutions. Among millennial Latinos (ages 18–35), 77% of respondents believed that Hispanics encounter discrimination. These results point to the importance of protecting consumers who remain outside the financial mainstream and for passing commonsense legislative solutions.

One potential policy reform is to expand access to financial advice, such as financial counseling programs. NCLR has a long history of advocacy and research in this area and has found that increasing financial knowledge among Hispanics is especially important given their relatively limited experience with financial tools. This commonsense policy solution also has considerable support from Latino voters. NCLR’s new economy poll found that 82% of respondents believe the federal government should support financial counseling for people who want to learn more about saving, how to budget, credit scores, or how to plan for retirement.

The FDIC report paints a mixed picture of improvements and setbacks for Latinos and makes it clear that NCLR’s work is not over. We will continue to meaningfully engage the Latino community in the mainstream financial system, support the Consumer Financial Protection Bureau’s work to advance consumer protections, and push for sound policy solutions.