ITIN Revalidation Process in Need of Streamlining

A new survey of NCLR Affiliates reveals challenges Certified Acceptance Agents face in assisting immigrants through the process

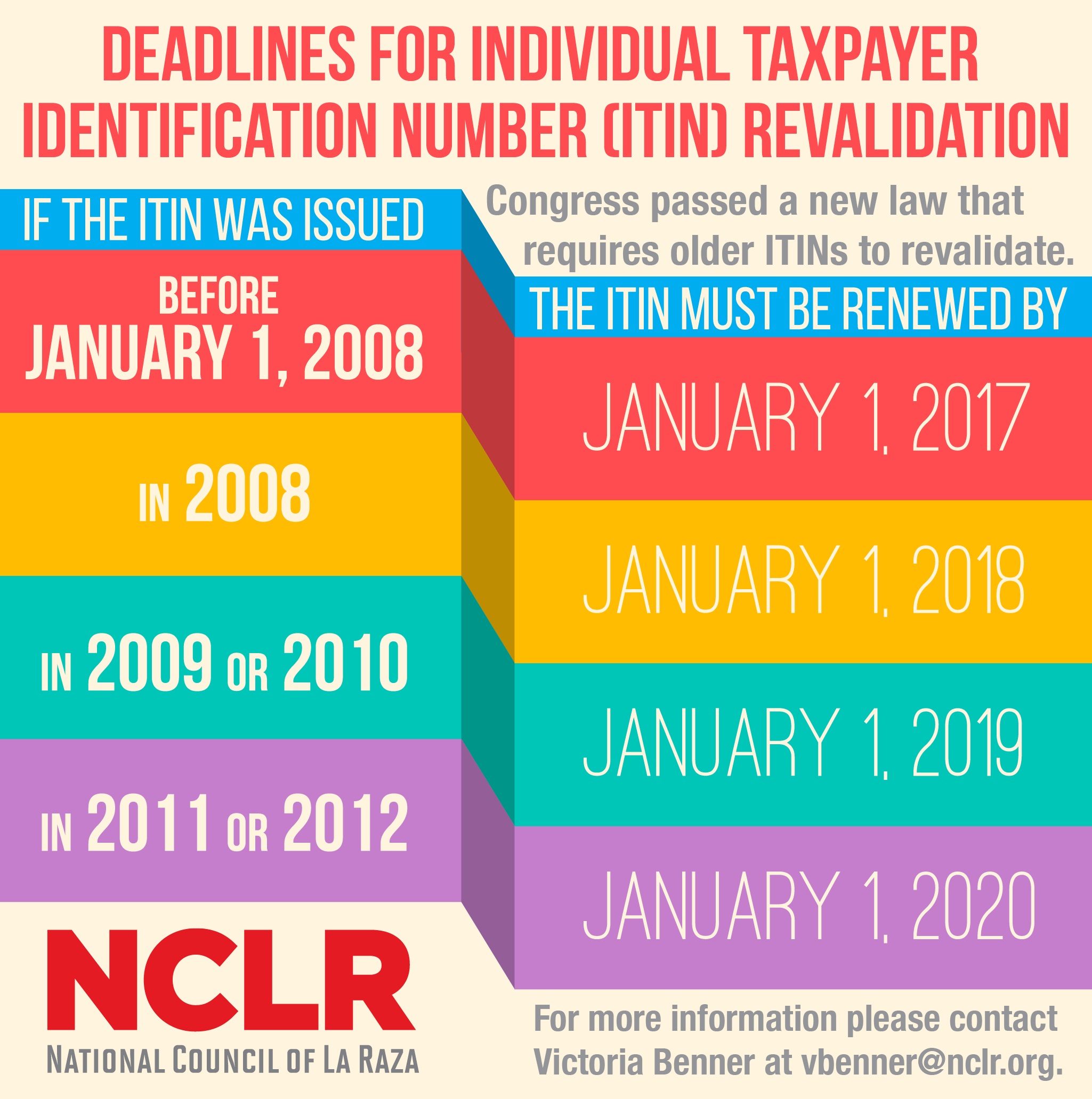

In the weeks ahead, the Treasury Department and the Internal Revenue Service (IRS) will implement a requirement enacted last December that immigrants with older Individual Taxpayer Identification Numbers (ITIN) must revalidate. The details of the revalidation process are not yet known but it is clear that Certified Acceptance Agents (CAAs) will be critical. CAAs are full-time staff, frequently at community-based tax preparers, providing immigrants with one-on-one assistance when applying for an ITIN.

One way that CAAs help is by certifying identity documents as originals and submitting an ITIN application on behalf of an immigrant. The IRS currently requires original identity documents—including birth certificates or passports—from immigrants applying for an ITIN. Once an application is submitted, it may take 10–14 weeks before these documents are returned with the ITIN.

Like most people, many immigrants are not comfortable being without these important documents for such a long time and fear that they will be lost in the mail. CAAs help make this process simpler and less daunting for taxpaying immigrants.

There is a sense of urgency to better understand some of the challenges in becoming a CAA to better assist immigrant taxpayers during the revalidation process.

Roughly seven million ITINs were issued before January 1, 2013, and will need to be revalidated over the next four years.

It is estimated that roughly three million renewals may be processed in the first year alone. To learn more about challenges, NCLR surveyed Affiliates and partners engaged in tax preparation and here is what we learned:

Staff Capacity: CAAs must be full-time staff, which is not always feasible for community-based organizations. However, there is very little funding available for community organizations to hire staff to become a CAA and existing staff is stretched thin on other projects. Further, many tax-preparers hire temporary staff or rely on volunteers to help with the tax-filing season.

Maintaining CAA Status: The application process to become a CAA is rigorous and maintaining the status is a challenge. Respondents shared that they must process five ITIN applications per year, which is not always possible for organizations new to tax preparation. In addition, the IRS must accept 90% of CAA-filed applications. Due to inconsistency at the IRS with processing ITIN applications and frequent rejections, failure to maintain this threshold is not necessarily demonstrative of quality.

Inconsistencies with ITIN Processing: There were a number of complaints about the uniformity of IRS staff training, accessibility, and communication. Some reported that an application was rejected and then accepted upon resubmission of the same application without changes. Additionally, medical and school records are allowed forms of identification, but are not always accepted. This is also the case with other valid forms of ID that may have expired, such as a driver’s license. As a result, a number of CAAs responded that they have a high rejection rate and it is not always clear why an application was rejected.

Given these challenges, some respondents noted that they chose not to apply to become a CAA or have pursued partnerships with other organizations instead. Understanding the importance of CAAs over the next four years, the IRS should streamline the application and compliance processes.

Adjusting CAA standards must be done in a way that preserves the program’s integrity but enables CAAs to continue their work and ensure that barriers to ITIN users are managed.