Latinos, Overrepresented in Small Businesses, Have Limited Access to Retirement Savings

By Ana Pupo, Public Policy Fellow, NCLR

Aside from Social Security, the most common way for the majority of Americans to save for retirement is through workplace payroll deductions into retirement plans. In fact, our country promotes saving for retirement with tax incentives that will amount to approximately $2 trillion over the next ten years. Unfortunately, about two-thirds of Latino workers won’t benefit from these generous tax incentives because they work for smaller companies that cannot afford to offer any type of retirement savings plan for their workers.

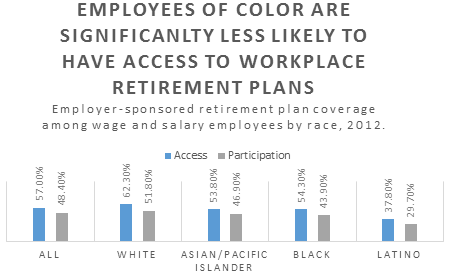

Overall, Latinos are far less likely to have dedicated retirement savings than Whites—almost 70 percent of Latinos do not have retirement accounts compared to less than 40 percent of White households. And while it’s essential that everybody save for retirement, it’s particularly prudent for Latinos to have their savings in order because they not only have longer life expectancies than their peers, but they also are a younger, rapidly growing segment of the American population. Without the necessary investments into retirement plans, Latinos will likely be forced to stretch every dollar of their retirement savings to ensure that those funds last longer than they might have expected.

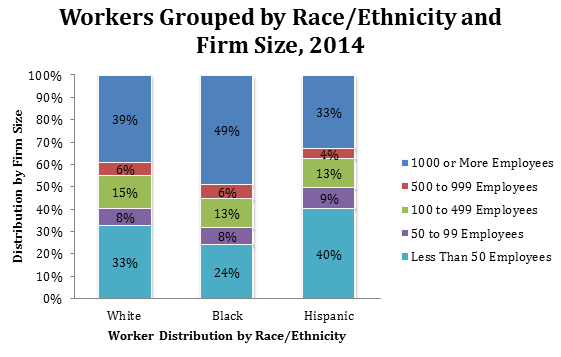

One complicating factor is that Latino workers are over-represented in small businesses that have fewer than 50 employees. Figure 1 demonstrates this “bottom-heavy” distribution.

Small employers operate with low profit margins and are often unable to offer benefits such as retirement plans. For instance, as of 2011, employers with fewer than 10 employees only sponsored retirement plans about 13 percent of the time, while firms with 10–49 employees did slightly better at 29 percent. In comparison, large businesses with over 1,000 employees offered these plans more than 65 percent of the time, and public sector employers did so over 79 percent of the time.

Economic downturns also force many small businesses to reduce employer contributions to savings or drop retirement plans altogether. It is no surprise, then, that recent trends show Hispanics have actually become less prepared for retirement over the past few years. Between 2002 and 2006, the share of Hispanics who participated in an employer-sponsored retirement plan in the private sector declined by an average annual rate of 0.9 percent.

Today, public policy discussions center on the economic pressures of the baby boomer generation. But given the demographic shift going on in this county, attainable retirement options for Latinos and other communities of color must also be addressed as lawmakers work to better secure the future of the nation’s aging population. What works for the next generation of retirees may not be a long-term solution to prevent future retirees, including far too many Latino workers, from being in a vulnerable position as they leave the workforce.