Small Steps to Revive the American Dream of Homeownership

President Obama recently gave a speech in Arizona announcing a reduction in mortgage insurance premiums charged by the Federal Housing Administration (FHA). This much-needed policy change will save homeowners with FHA loans an average of $900 a year on their mortgage payments while making the dream of homeownership more affordable and easier to reach for many Americans, including Latinos.

President Obama recently gave a speech in Arizona announcing a reduction in mortgage insurance premiums charged by the Federal Housing Administration (FHA). This much-needed policy change will save homeowners with FHA loans an average of $900 a year on their mortgage payments while making the dream of homeownership more affordable and easier to reach for many Americans, including Latinos.

Unfortunately, the key message and potential benefits to hard-working Americans were lost following the announcement. Conservative policymakers were quick to invoke a deeply entrenched false narrative that attributes the collapse of the housing market to unqualified borrowers. For example, House Financial Services Committee Chairman Jeb Hensarling (R–Texas) released a statement calling the reduction in FHA premiums disappointing and warned against “the destructive cycle of boom, busts, and bailouts that poor decisions in Washington produce.

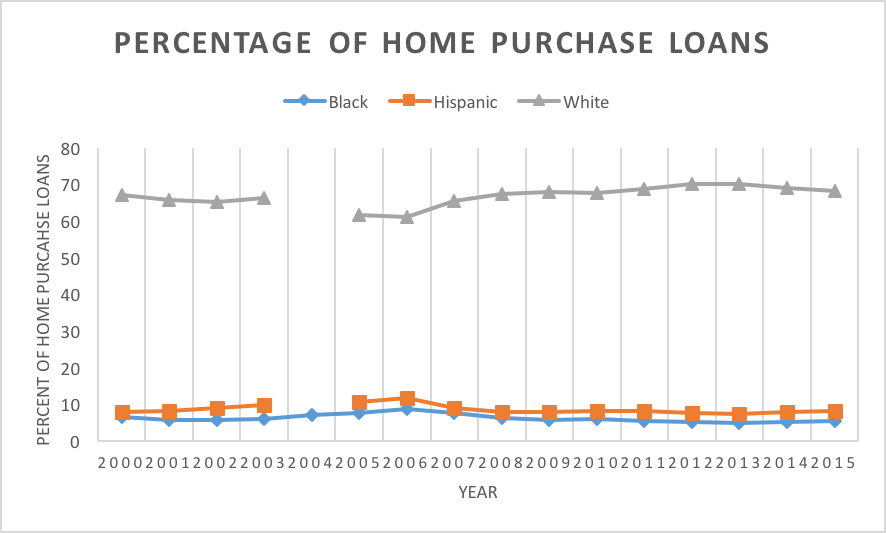

Regrettably, comments like this from Hensarling and others distract from the large body of evidence confirming that the foreclosure crisis was a result of unscrupulous lenders steering minority borrowers into costly subprime loans. The Financial Crisis Inquiry Commission, studies by economists at the Federal Reserve, and a number of other independent investigations have all shown that the housing crisis stemmed from private-sector lenders chasing profits by producing large volumes of unsustainable loans without regard for borrowers. The Department of Justice reached historic settlements with large lenders charged with steering Black and Hispanic borrowers into predatory subprime products, even when these borrowers qualified for safer conventional mortgages. Additionally, a recent study by a private consulting firm refutes the idea that mortgage credit was easily attainable leading up to the housing market’s collapse. Using 10 years of mortgage originations, the study finds denial rates were actually higher before the crisis than they are in today’s tight credit market. Yet, just as banks and other financial institutions received taxpayer bailouts, they responded by restricting access to affordable mortgage credit to only the most pristine borrowers.

This restrictive environment is where we find ourselves today. Access to affordable mortgage credit continues to be a real barrier to homeownership, especially for qualified Latinos and other underserved markets. The reduction in mortgage insurance premiums from the FHA is expected to provide some relief to put many qualified Americans on the path to homeownership and better financial prospects. We hope that in the future, policymakers stop blaming victims of the foreclosure crisis and we encourage the Obama administration to continue doing more to put the dream of homeownership back within reach of Latino families.