In Fannie Mae and Freddie Mac Overhaul, Don’t Leave Out Latino Families

(This was originally posted to the Home for Good blog.)

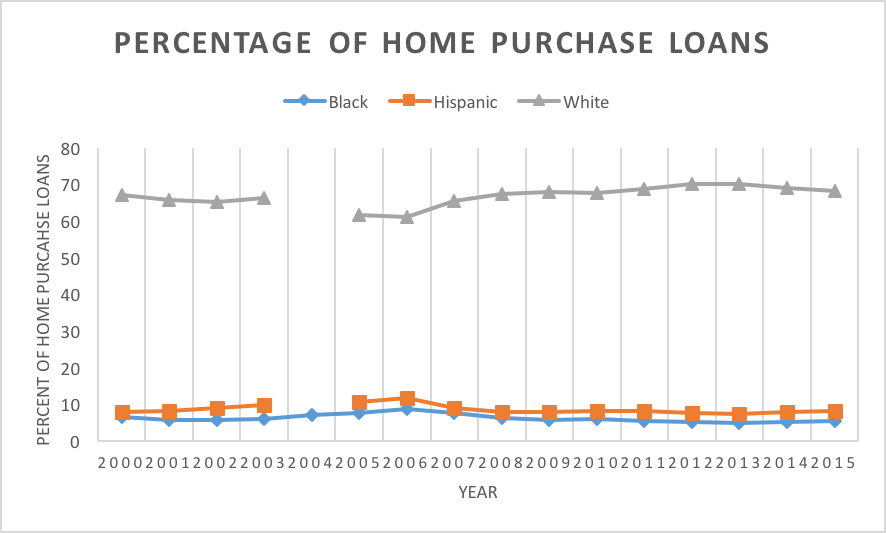

![]() Last week, the Senate Banking Committee announced a new bipartisan agreement to overhaul our nation’s housing finance system by restructuring government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac. The draft discussion bill, authored by Committee Chairman Tim Johnson (D-S.D.) and Ranking Member Mike Crapo (R-Idaho) (Johnson-Crapo), preserves the 30-year fixed mortgage and takes concrete steps to prevent a future housing crisis.

Last week, the Senate Banking Committee announced a new bipartisan agreement to overhaul our nation’s housing finance system by restructuring government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac. The draft discussion bill, authored by Committee Chairman Tim Johnson (D-S.D.) and Ranking Member Mike Crapo (R-Idaho) (Johnson-Crapo), preserves the 30-year fixed mortgage and takes concrete steps to prevent a future housing crisis.

While we welcome these meaningful steps toward sustainable housing finance reform, the Johnson-Crapo draft contains shortcomings that reduce affordable access to credit for Latino families and underserved communities.

Under the proposed system, Fannie Mae and Freddie Mac would be dissolved and replaced with private capital overseen by a new government-backed mortgage-bond insurer and regulatory agency called the Federal Mortgage Insurance Corporation (FMIC).

Modeled after the FDIC, which insures bank deposits, the FMIC would provide a government guarantee for mortgages while private firms would be required to accept losses of up to 10 percent of capital. In exchange for the guarantee, firms would pay a small 0.1 percent fee on all mortgage securities to fund affordable housing and community development. This small fee would finally fund the National Housing Trust Fund and the Capital Magnet Fund, two essential affordable housing programs that NCLR has long advocated for. These funds have the potential to make significant, much-needed investments in affordable housing, yet they have never been funded since their inception more than five years ago.

Though the bill contains numerous bright spots for the Latino community, Johnson-Crapo also removes beneficial features that exist in the current housing finance system under Fannie Mae and Freddie Mac. These features should be reworked in the Johnson-Crapo proposal to make affordable housing a real priority for housing finance reform.

Though the bill contains numerous bright spots for the Latino community, Johnson-Crapo also removes beneficial features that exist in the current housing finance system under Fannie Mae and Freddie Mac. These features should be reworked in the Johnson-Crapo proposal to make affordable housing a real priority for housing finance reform.

One example is that Fannie Mae and Freddie Mac maintain a “duty to serve” the entire housing market, and as part of their public mission, they are required to provide financing for affordable housing. In contrast, the Johnson-Crapo system replaces this duty to serve and its affordability goals with an incentive-based fee structure to fund affordable housing programs. This mechanism, while creative, may not sufficiently address our current and future affordable housing needs. The fee can be raised or lowered based on how well entities perform in lending to underserved borrowers, but the criteria for who is considered high-performing is unclear. This could lead to the housing market not adequately serving the Latino community.

With regard to fair housing and fair lending, Johnson-Crapo does not explicitly prohibit involved entities from discrimination based on race, gender, national origin, familial status, and other characteristics. Failing to include such statements, combined with a lack of a strong regulatory body and transparency requirements, could create a recipe for failure to achieve fair lending that is free of discrimination.

Finally, the proposal does not incorporate the proven benefits of housing counseling in a post-GSE landscape. Research shows that homeowners who work with qualified housing counselors are less likely to be delinquent on their mortgages. When faced with foreclosure, they’re more likely to receive modifications. If the FMIC replaces the GSEs, the new agency should integrate housing counseling into its programs.

As debate begins on the merits of the Johnson-Crapo bill, Congress should not forget that a strong and sustainable commitment to fair lending and affordable housing is crucial to the well-being of not just the Latino community and other underserved groups, but the entire economy. Communities of color were affected most severely during the housing crisis, and they deserve a chance to rebuild what was lost. More importantly, these communities are the future of the housing market. If it is going to succeed, the new housing system cannot shut them out.