Exciting Changes Coming for Latino Families in the Housing Market

By Nancy Wilberg Ricks, Senior Policy Communications Strategist, NCLR

Today, the Consumer Financial Protection Bureau (CFPB) launched its long-awaited mortgage servicing standards and qualified mortgage (QM) rules. These comprehensive changes will significantly improve the mortgage market. First, the new servicing standards will ensure that servicers are accountable for the loans they administer and bring order to a wildly inconsistent third-party system. Second, the QM rule has done away with many types of unsustainable loan characteristics and will ensure that the rights of future buyers are no longer overlooked in the home-buying process. Unique to these rules are their longevity. While Washington has implemented numerous fixes in response to the housing crisis, these new rules are lasting solutions that we hope will steer the nation far from the repeat of a housing bubble.

Today, the Consumer Financial Protection Bureau (CFPB) launched its long-awaited mortgage servicing standards and qualified mortgage (QM) rules. These comprehensive changes will significantly improve the mortgage market. First, the new servicing standards will ensure that servicers are accountable for the loans they administer and bring order to a wildly inconsistent third-party system. Second, the QM rule has done away with many types of unsustainable loan characteristics and will ensure that the rights of future buyers are no longer overlooked in the home-buying process. Unique to these rules are their longevity. While Washington has implemented numerous fixes in response to the housing crisis, these new rules are lasting solutions that we hope will steer the nation far from the repeat of a housing bubble.

The servicing standards in particular are critical to true recovery for Latino households and will bring accountability to the loss mitigation system by streamlining processes for both families and servicers. NCLR and allies pushed the CFPB to make the new standards as efficient and strong as possible to avoid the proliferation of harmful servicing practices. In particular, the issue of dual tracking—the practice of processing a family through foreclosure while they are simultaneously considered for a loan modification—is one essential fix in the new standards. The rules also require that before foreclosing on a family, servicers must work through proper and legitimate channels, maintain and provide accurate documentation, and make good-faith efforts to help a homeowner through loss mitigation opportunities.

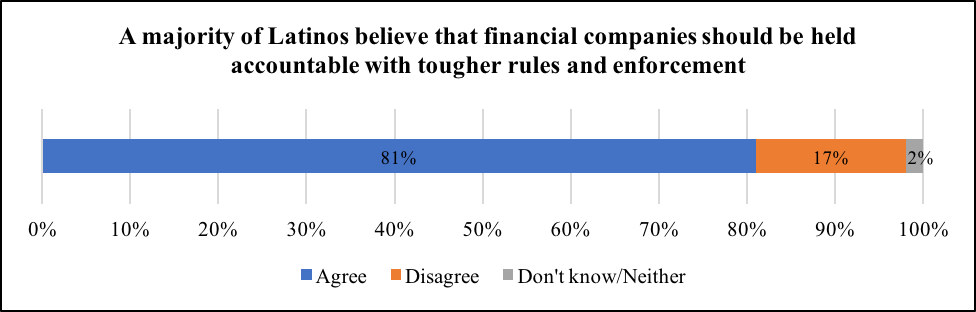

Communities of color have been long plagued by discriminatory practices both when purchasing a home and when striving to save their home from unnecessary foreclosure. Studies indicate that Latino and Black homeowners were more likely to receive high-risk and costlier mortgages than their White counterparts despite having comparable credit profiles. Communities of color still struggle to stabilize their neighborhoods even six years after the crisis. The new QM rule offers strong protections against discriminatory and predatory practices, and with reasonable flexibility so as to not stifle credit access. The new rule will halt practices that set Latino families back from decades of progress in wealth accumulation and home values. We are encouraged that the CFPB’s provisions will finally put homeowners back on the path to recovery; indeed, the banks may have recovered, but our families have not benefitted from the same relief.

The CFPB is reaching out far and wide to put the mortgage industry on notice and ensure that homeowners know their rights. Since the rules were finalized last January, the CFPB has worked closely with lenders to make sure they’re ready for the launch of the new QM and servicing standards rules. They also designed a dedicated web page for homeowners as well as user guides and in-person trainings for community organizations that are on the front lines of helping families save their homes. Finally, the CFPB Director, Richard Cordray, has taken media spots such as this one on The Daily Show (below) to alert the nation that accountability to consumers is here to stay.

The Daily Show

Get More: Daily Show Full Episodes,The Daily Show on Facebook

While NCLR and its consumer and civil rights partners expect great things from these changes, there is more that needs to be done to protect consumers who are still struggling to recover from the recession. Progress will be made not only through the rules’ implementation but also in their enforcement to ensure that that there is finally true accountability in the mortgage finance system.