Low-income Borrowers & Minorities Need Other Sources of Mortgage Credit

By Enrique Lopezlira, Senior Policy Advisor, NCLR Policy Analysis Center

The financial health of the Mutual Mortgage Insurance Fund, a fund that insures mortgages made by the Federal Housing Administration (FHA) on single-family homes, has improved substantially, according to a recent report by the agency. Although the fund is still in the negatives, FHA expects the fund to meet its 2 percent capital reserve ratio by 2015—two years earlier than predicted by an independent actuary last year.

The financial health of the Mutual Mortgage Insurance Fund, a fund that insures mortgages made by the Federal Housing Administration (FHA) on single-family homes, has improved substantially, according to a recent report by the agency. Although the fund is still in the negatives, FHA expects the fund to meet its 2 percent capital reserve ratio by 2015—two years earlier than predicted by an independent actuary last year.

This improvement is more impressive when considering the countercyclical role FHA played during the housing crisis. FHA saw its share of the housing market balloon fivefold during this time. As private capital fled the industry, FHA continued to ensure that families had access to mortgage credit. By carrying out this role, FHA prevented a further erosion of both housing prices and jobs.

The fund’s current financial improvement is the result of a comprehensive approach by FHA to restore financial stability to the fund, so that it is available again during the next economic downturn. But the success of this approach has unintended consequences: a tightening of credit for low-income borrowers and communities of color.

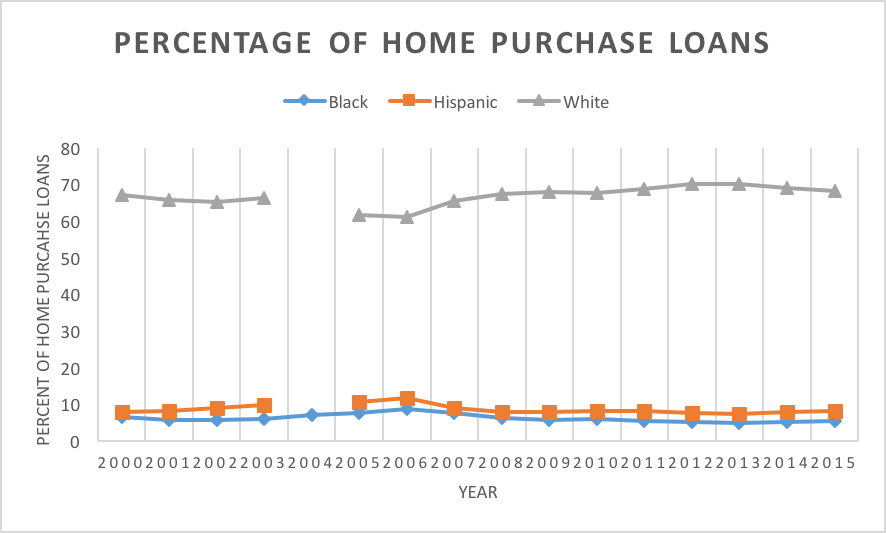

Over the past three years, FHA-insured mortgages have become more and more expensive. Increases in mortgage insurance rates and down payment requirements, along with requirements to carry mortgage insurance throughout the life of a loan, have put FHA loans out of reach for many creditworthy low- and middle-income borrowers. Furthermore, FHA announced last week that it would significantly decrease loan limits starting January 1, 2014, in an effort to cut back its market share and lure private capital back to the mortgage sector. This policy will make it even more difficult for Hispanic borrowers to get an FHA loan, especially in high-priced areas, such as many parts of California. Without an FHA option, borrowers will have to rely on private capital, but private capital generally serves the cream of the crop (borrowers with high income, high down payments, and high credit scores), not low-income borrowers with low down payments.

What does this mean? It means that while part of FHA’s mission is aiding low-wealth households in accessing mortgage credit, FHA cannot be the only lender for borrowers in low-income areas and communities of color. The housing market needs comprehensive reform, and this reform must ensure that all creditworthy borrowers have access to affordable mortgage credit. It’s neither efficient nor optimal to expect FHA to serve these markets alone.