Are Big Banks Keeping Their Promises to Homeowners?

New Report Highlights Mixed Compliance

By Janis Bowdler, NCLR; Cy Richardson, National Urban League; and Lisa Hasegawa, National CAPACD

On Wednesday, we got an inside look into whether or not the big banks have kept their promise to our families. National Mortgage Settlement Monitor Joseph A. Smith, Jr. released his compliance report which details how the five largest banks that entered into a $25 billion settlement on account of fraudulent robo-signing have carried out their end of the bargain. The results are mixed.

While the settlement has brought greater transparency to the banks’ activities—something that will lay the tracks for greater accountability as we work to reform the housing market—our families have not received all the relief we hoped they would. Some have compared the settlement relief with winning the lottery. Very few win, but when they do, they win big.

We at the Alliance for Stabilizing Our Communities—a partnership between the National Council of La Raza (NCLR), the National Urban League, and the National Coalition for Asian Pacific American Community Development—have carefully tracked the banks’ activity under the settlement. We hosted a summit featuring Monitor Smith in February voicing our concerns that communities of color are the least likely to receive relief, though study after study indicates that they were the hardest hit by the banks’ practices. We have also sent the monitoring committee a steady stream of on-the-ground reports from our housing counselors who hear directly from families in their neighborhoods.

Wednesday’s report from Monitor Smith offers an examination of whether banks are making good on their promise to the 49 states who entered the agreement. According to the parameters that Monitor Smith is using, the banks have complied with several but not all points. For example, according to the report, all five banks have stopped charging distressed borrowers an application fee just to process a loan modification request. On the other hand, banks are not meeting proper timelines when collecting loan modification documents. Monitor Smith has recommitted to ensuring this is rectified. Indeed, we hope to see vast improvement in this area, as many know all too well that a mere paperwork glitch can make the difference in saving one’s home or not.

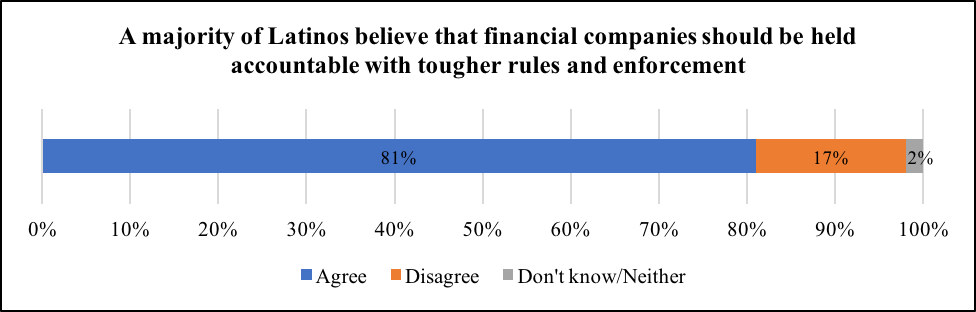

This settlement must be the beginning of a sea change. While on the recovery trail, the landmark settlement shed light on the harmful servicing practices that were running rampant throughout the nation. That’s a start. In addition, we continue to witness the release of strengthening and lasting regulations coming out of the Consumer Financial Protection Bureau (CFPB). The CFPB deployed greatly improved servicing standards in the regulations it published in January. These are all critical steps in an essential culture change. While the crisis highlighted damaging lending practices, they were no surprise to communities of color for whom such barriers are an everyday part of their financial lives. Our families have long been targeted by predatory market players and it is time to see a sweeping change for all.